When starting a project, the data scientist focuses on exploration and experimentation, rather than turning the process into an immediate production system. This notebook presents a simplified view of this stage.

Resources

The following resources are used as part of this tutorial:

data

data/seattle_housing_col_description.txt: Describes the columns used as part data analysis.

data/seattle_housing.csv: Sample data of the Seattle, Washington housing market between 2014 and 2015.

code

postprocess.py: Formats the data after inference by the model is complete.

preprocess.py: Formats the incoming data for the model.

simdb.py: A simulated database to demonstrate sending and receiving queries.

wallaroo_client.py: Additional methods used with the Wallaroo instance to create workspaces, etc.

Model Testing: Evaluate different models and determine which is best suited for the problem.

Import Libraries

First we’ll import the libraries we’ll be using to evaluate the data and test different models.

importnumpyasnpimportpandasaspdimportsklearnimportsklearn.ensembleimportxgboostasxgbimportseabornimportmatplotlibimportmatplotlib.pyplotaspltimportsimdb# module for the purpose of this demo to simulate pulling data from a databasematplotlib.rcParams["figure.figsize"] = (12,6)

# ignoring warnings for demonstrationimportwarningswarnings.filterwarnings('ignore')

Retrieve Training Data

For training, we will use the data on all houses sold in this market with the last two years. As a reminder, this data pulled from a simulated database as an example of how to pull from an existing data store.

Only a few columns will be shown for display purposes.

conn=simdb.simulate_db_connection()

tablename=simdb.tablenamequery=f"select * from {tablename} where date > DATE(DATE(), '-24 month') AND sale_price is not NULL"print(query)

# read in the datahousing_data=pd.read_sql_query(query, conn)

conn.close()

housing_data.loc[:, ["id", "date", "list_price", "bedrooms", "bathrooms", "sqft_living", "sqft_lot"]]

select * from house_listings where date > DATE(DATE(), '-24 month') AND sale_price is not NULL

id

date

list_price

bedrooms

bathrooms

sqft_living

sqft_lot

0

7129300520

2023-07-31

221900.0

3

1.00

1180

5650

1

6414100192

2023-09-26

538000.0

3

2.25

2570

7242

2

5631500400

2023-12-13

180000.0

2

1.00

770

10000

3

2487200875

2023-09-26

604000.0

4

3.00

1960

5000

4

1954400510

2023-12-06

510000.0

3

2.00

1680

8080

...

...

...

...

...

...

...

...

20518

263000018

2023-03-08

360000.0

3

2.50

1530

1131

20519

6600060120

2023-12-11

400000.0

4

2.50

2310

5813

20520

1523300141

2023-04-10

402101.0

2

0.75

1020

1350

20521

291310100

2023-11-03

400000.0

3

2.50

1600

2388

20522

1523300157

2023-08-02

325000.0

2

0.75

1020

1076

20523 rows × 7 columns

Data transformations

To improve relative error performance, we will predict on log10 of the sale price.

Predict on log10 price to try to improve relative error performance

Now we pick variables and split training data into training and holdout (test).

vars= ['bedrooms', 'bathrooms', 'sqft_living', 'sqft_lot', 'floors', 'waterfront', 'view',

'condition', 'grade', 'sqft_above', 'sqft_basement', 'lat', 'long', 'sqft_living15', 'sqft_lot15', 'house_age', 'renovated', 'yrs_since_reno']

outcome='logprice'runif=np.random.default_rng(2206222).uniform(0, 1, housing_data.shape[0])

gp=np.where(runif<0.2, 'test', 'training')

hd_train=housing_data.loc[gp=='training', :].reset_index(drop=True, inplace=False)

hd_test=housing_data.loc[gp=='test', :].reset_index(drop=True, inplace=False)

# split the training into training and val for xgboostrunif=np.random.default_rng(123).uniform(0, 1, hd_train.shape[0])

xgb_gp=np.where(runif<0.2, 'val', 'train')

# for xgboost, further split into train and valtrain_features=np.array(hd_train.loc[xgb_gp=='train', vars])

train_labels=np.array(hd_train.loc[xgb_gp=='train', outcome])

val_features=np.array(hd_train.loc[xgb_gp=='val', vars])

val_labels=np.array(hd_train.loc[xgb_gp=='val', outcome])

Postprocessing

Since we are fitting a model to predict log10 price, we need to convert predictions back into price units. We also want to round to the nearest dollar.

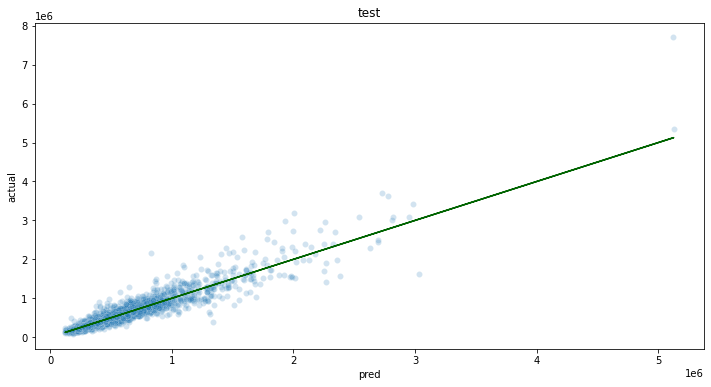

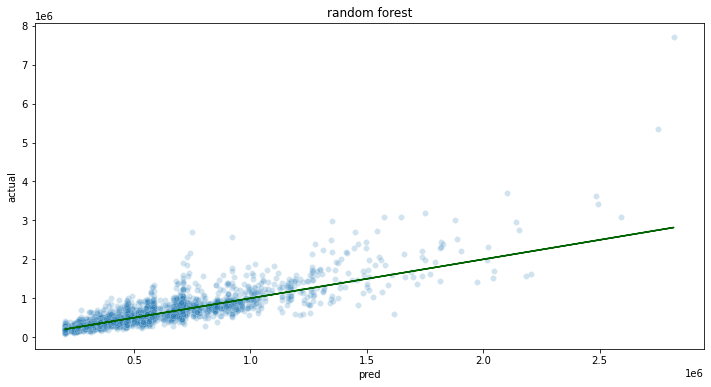

For the purposes of this demo, let’s say that we require a mean absolute percent error (MAPE) of 15% or less, and the we want to try a few models to decide which model we want to use.

One could also hyperparameter tune at this stage; for brevity, we’ll omit that in this demo.

In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook. On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook. On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.